The multifamily sector now is the strangest in my fairly short job (12 yrs). The range of likely financial outcomes is broad, and I undoubtedly lack the expertise to evaluate the effects inflation, fees, and a economic downturn may possibly have on the multifamily sector about the close to-phrase.

What is good about obtaining this outlet is that I get to create factors down and consider out loud, documenting my views and executing my ideal to make perception of the sector.

Though admittedly I’m not sure what’s heading to come about, the over-made use of adage rings accurate – whilst historical past may not repeat by itself, it does rhyme.

Let’s split matters down into a couple distinctive segments inflation/premiums, solitary-household housing, offer/need fundamentals, and thoughts/points to check out.

Inflation / Premiums

Real estate, and multifamily in certain, is a superior inflation hedge. Rents reset day-to-day, and leases usually roll every 12 months. Hire growth at our existing houses have considerably outpaced inflation.

Despite the fact that inflation fears are higher today, the consensus is that it will be tamed, but at what value?

Provided inflation is a fairly limited-time period concern, the sector is reacting far more acutely to the rise in interest premiums. The surge in borrowing fees have driven up cap prices and introduced the capital marketplaces to a momentary freeze. This has been most noteworthy on benefit-add specials the place buyer’s commonly set on higher leverage.

I assume rates to keep on being higher, but normalize and come again down as economic downturn fears set in. Spreads need to also stabilize as we get additional clarity on the market path.

Solitary-Family members Housing

The solitary-family housing market is terribly unhealthy these days. Logan Mohtashami from HousingWire has the some of the clearest housing examination which goes like this (based mostly on this article):

- The run up in housing price ranges in excess of the past 2 a long time has been pushed primarily by inventory becoming at all-moments lows at a time when housing demographics have been very solid.

- Stock has been steadily falling since 2014 and is in an unhealthy place nowadays. Typically stock degrees are in between 2 million and 2.5 million. We started out 2022 at just 870,000 residences for sale.

- A career-loss recession would be essential to make any sort of distress. Nevertheless, the buyer is in a solid economical placement currently.

- Higher rates will gradual housing need and we’re now seeing obtain purposes slowing, but it is going to just take a whilst for stock degrees to enhance considerably.

Unaffordable housing is a boon for multifamily demand in the small-phrase, but more than the very long-expression bigger fees will sluggish housing desire and moderate pricing, hence building one-family members housing much more cost-effective.

The Renter

American people reman in great financial overall health owing to the mix of a strong labor industry, wage development, low leverage, and operate up in housing price ranges and the stock market.

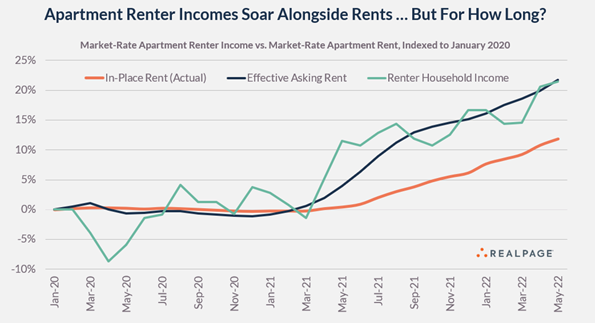

Just one of the biggest drivers and one particular of the major question marks now is what happens to renter domestic incomes goin ahead. When I wrote about the SE multifamily sector back in January, I requested ‘are rents outpacing wages in these marketplaces to these an lengthen that there are not plenty of high-shelling out jobs to assistance them?’

That stays the major question about the multifamily sector today. Incomes and rents are intently corelated. As charges continue on to surge, most notably payroll, insurance policies, utilities, R&M, and taxes, there remains stress to thrust rents.

If wage growth stagnates, we’ll see much more doubling up, lower retention, and a reduction in new lease demand from customers. See the chart down below from Jay Parsons of RealPage exhibiting the limited correlation concerning incomes and rents.

Multifamily Supply/Need

Desire

The multifamily fundamentals stay solid. Job development and wage advancement are both of those predicted to keep on being healthy. Moreover, the uncoupling of youthful older people from moms and dads and roommates will keep on to advantage in close proximity to term demand from customers. However, the demographics soften as the 25–34-12 months-outdated cohort grows at <0.5% per year over the next 3 years, then declines starting in 2025 (Green Street).

Additionally, the recent rise in rates and the likely impending recession may lead to hiring freezes and layoffs in certain sectors, resulting in slower than expected job growth.

Revenue growth will continue to be strong due to mark-to-market of the rent roll (especially in the Sunbelt) but will likely slow due to deteriorating macroeconomic conditions.

Supply

On the supply side, development delays have helped insulate apartment fundamentals. However, supply will grow over the coming years as the units under construction eventually deliver and the starts/permits continue to accelerate.

Tightening credit markets and rising construction costs may restrain supply in the short-term, but rising rents (and attractive profit margins) will keep a floor under starts.

Supply will vary by market with the Sunbelt markets seeing accelerating supply growth over the next 2-3 years. There are no absorption issues today, and broad-based excesses in supply are unlikely in the near-term given the strong demand, but select markets are heading for over-supply.

Questions/Things to Watch

- Are we heading for a recession and if so, how severe will it be?

- Will the labor market remain tight and will wage growth continue?

- Will supply catch up to demand and are select markets over-supplied?

- Are rents outpacing wage growth, leading to expanding rent-to-income ratios?

- Will rates normalize then begin to decline as recession fears set it?

- When will supply-chain issues taper and will construction costs come back down any time soon?

While this is my attempt of making sense of today’s market, I remain focused on buying and building multifamily assets to hold long-term in markets with strong fundamentals.