Key News

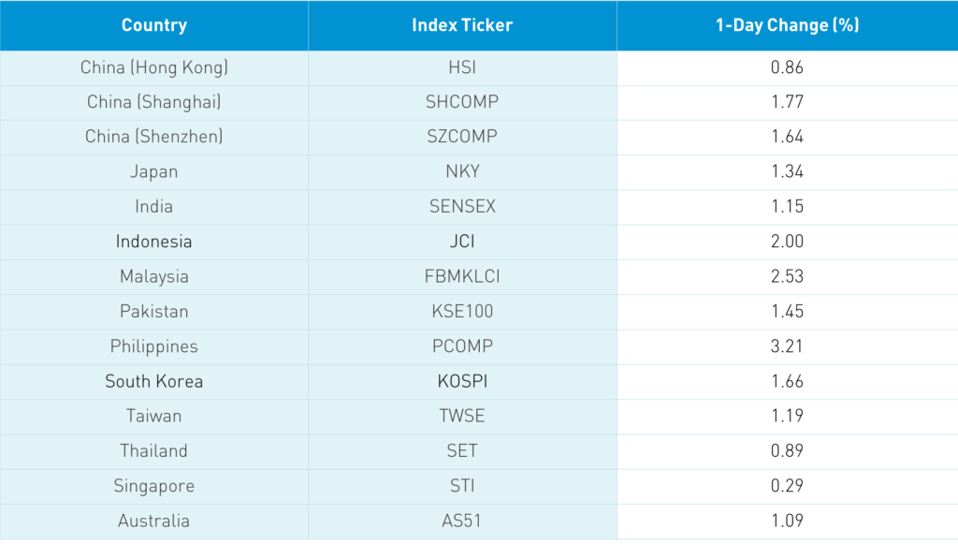

Yesterday’s MSCI

Hong Kong volume leaders were Meituan, which fell -0.28% post-earnings yesterday as analysts debate future growth rates, Tencent, which rose +2.66% on buying by Mainland investors via Southbound Connect, Alibaba

Trip.com (TCOM US) reports after the US close today.

We will have further commentary on the potential House vote tomorrow, which would force US-listed Chinese companies to allow the PCAOB to review their audit books, which the Chinese law does not allow. 100% of the Chinese companies should adhere to this global standard, though a resolution is far more likely to occur under a Biden administration than under Trump. Additionally, the SEC has outlined a path for a resolution. The headlines might not be encouraging but I don’t believe anyone wants the companies to face delisting, which wouldn’t occur for three years. When the Senate passed its delisting bill, the market sold off but very quickly rebounded. Remember to watch CNH, China’s currency price during US trading hours, as an indicator. I assume that it may fluctuate on the news but as we saw this spring, it quickly rebounded.

Social media platform Momo (MOMO US) reported earnings before the US market open today, which beat lower analyst expectations. The online video space has been hurt by strong competition for advertising dollars due to Bytedance (this is true in the US as some element of TikTok criticism from Facebook is due to its competitive threat) and the potential for regulation. Social media companies have faced the headwind of traditional retailers scaling back advertising as well. Expectations were very low, which the company beat while investors focus on e-commerce’s strength.

- Revenues -15.4% to $554mm (RMB 3.766B) versus Q3 2019’s RMB 4.451B analyst estimate of RMB 3.711B

- Adjusted net income $96mm (RMB 456mm) versus Q3 2019’s RMB 1.084B analyst estimate of RMB 570mm

- Adjusted EPS $0.44 (RMB 2.98) versus Q3 2019’s RMB 4.90 analyst estimate of RMB 2.52

- Q4 revenue forecast is down -22% to -20%

kraneshares

Takeaway: The Caixin Manufacturing PMI, conducted by IHS Markit, hit its highest level in a decade, led by “a sharp and accelerated rise” from manufacturing companies. Sales expanded at “the quickest rate for a decade, which was often linked to a rebound in client demand.” The commentary from IHS Markit noted that domestic demand, as opposed to exports, was the driver. We had a strong uptick in employment, which grew for the third straight month. The strength in both depth and breadth of today’s release are quite impressive. While the market was overshadowed by trading due to MSCI’s Semi-Annual Index Review, yesterday’s strong “official” PMIs Dr. Copper did not ignore it, rising +2.34% yesterday in trading on the Shanghai Futures Exchange and tacking on another +0.83% overnight. I’ve previously mentioned that I like technical analysis because it takes the emotions driven by headlines out of the investment process. Copper is screaming about China’s V-shaped recovery. Don’t trust me, but check out the chart.

kraneshares

kraneshares

Upcoming Events

Sign up for KraneShares Model Portfolios to view our next webinar: Insights in Action – Asset Class Specialization in Emerging Markets and China is the Key to Differentiated Returns Today, December 1st, 11:00 am – 12:00 pm EST.

Click here to register!

H-Share Update

The Hang Seng opened and stayed in a tight range all day, closing up+0.77%/+122 index points at 26,567. Volume plunged by -36% from yesterday, though still 124% of the 1-year average while breadth had 27 advancers and 22 decliners. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +1.33%, led by financials +2.75%, communication +2.33%, staples +1.59%, materials +1.42%, and industrials +1.08%, while energy fell -1.49% and tech -0.61%. Southbound Stock Connect volumes were light/moderate as Mainland investors bought $633mm of Hong Kong stocks as Southbound Connect trading accounted for 10.3% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gained +1.77% and +1.64% to close at 3,451 and 2,286 respectively. Volume was off -8% from yesterday, which is 105% of the 1-year average while breadth was strong with 3,134 advancers and 590 decliners. The 522 Chinese stocks within the MSCI China All Shares Index gained +2.09%, led by financials +3.22%, communication +3.01%, healthcare +2.93%, industrials +2.15%, and discretionary +1.93%. Northbound Stock Connect volumes were moderate/high as foreign investors bought $2.479B of Mainland stocks today as Northbound trading accounted for 5.9% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.57 versus 6.58 yesterday

- CNY/EUR 7.87 versus 7.89 yesterday

- Yield on 1-Day Government Bond 1.00% versus 1.20% yesterday

- Yield on 10-Year Government Bond 3.27% versus 3.25% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.70% yesterday

- China’s Copper Price +0.70% overnight

About KraneShares

Krane Funds Advisors, LLC is the investment manager for KraneShares ETFs. Our suite of China focused ETFs provide investors with solutions to capture China’s importance as an essential element of a well-designed investment portfolio. We strive to provide innovative, first to market strategies that have been developed based on our strong partnerships and our deep knowledge of investing. We help investors stay up to date on global market trends and aim to provide meaningful diversification. Krane Funds Advisors, LLC is majority owned by China International Capital Corporation (CICC).