Khanchit Khirisutchalual/iStock via Getty Images

You bet there is, and I will touch on what real estate investors need to know shortly, but first, let us review the following.

We follow the US and Canadian real estate markets closely. Real estate is a very slow-moving asset, and it’s not always that exciting. When we receive our monthly rental property checks each month, it’s almost as boring as watching paint dry.

But, any wise investor knows that consistent and sustainable wealth is built over time and pays huge dividends down the road. This means that in 10 – 20 years, the rental properties will be paid off by the renters. The home values will be 1-4x more valuable, and it provides cash/income for life.

I invest in real estate and think it’s one of the best long-term investments, beating out the stock market if you were to factor in risk/volatility. But there are times when buying real estate is not so good, and 2022 is one of those years.

In one month, real estate fell 14.7% in parts of Canada and the USA. In fact, the IYR real estate ETF fell 15% as well which helps confirm this during the same time window.

Here is some proof from the town where Technical Traders Ltd. is based.

My question to you is if you think it is wise to pay all-time highs for a property or wait for another 15-25% correction before investing in a new home or rental property?

High-level view of investing in 2022

The US stock market contracted sharply in early 2022 while traders attempted to identify the risks associated with the US Fed rate increase. Behind the scenes, real estate investors and homeowners are under pressure due to higher costs on nearly everything. Gas, food, everyday items, credit card interest payments – almost everything costs more due to inflation and increasing fuel costs.

I remember in 2007-08 when Oil reached levels above $140ppb and the seemingly high costs of everything just before inflation peaked and the markets turned bearish. Back then, much like today, a period of extreme speculation seemed to permeate buyers and investors throughout the US.

What broke this trend was the Global Financial Crisis. When the economy started to unravel, excessive credit/debt levels suddenly became unmanageable for nearly everyone. What seemed like a reasonable and manageable amount of debt suddenly became excessive as the US Fed raised the Fed Funds rate from 1.0% to 5.5% – a 450% increase.

Recently, we’ve seen the US Federal Reserve raise rates from 0.25% to 1.0%. The Fed may raise rates again soon, trying to tame inflation. I don’t have a crystal ball, but it is not difficult to understand how inflation, higher consumer costs, and increased debt servicing costs are going to panic many real estate investors, especially after many years of ZIRP and low inflation.

Real estate investors and homeowners burdened by higher costs & dwindling incomes

US investors are struggling to manage their finances as inflation and higher cost of living expenses continue to eat away their extra cash. Remember, what happens on a consumer/retail level is often the “canary in the coal mine” type of scenario related to broader economic trends. As consumers shift their spending habits, news travels quickly to other consumers about how the economic conditions are threatening their future.

The extreme measures taken when COVID-19 hit in February 2020 helped many real estate investors and homeowners, and consumers survive the extreme economic contraction that took place. Now that we are beyond extreme measures, prices have risen more than 25% over the past 24+ months for almost everything. Investors are struggling to manage their monthly expenses while still trying to enjoy their lifestyles.

A recent article highlighting former Federal Reserve Chairman Ben Bernanke suggests the current US Fed waited too long to address inflation issues. The steps now necessary to tame inflation could be very painful going forward. I see this as a very clear warning for traders/investors to keep their assets very liquid and to reduce their exposure to risk factors.

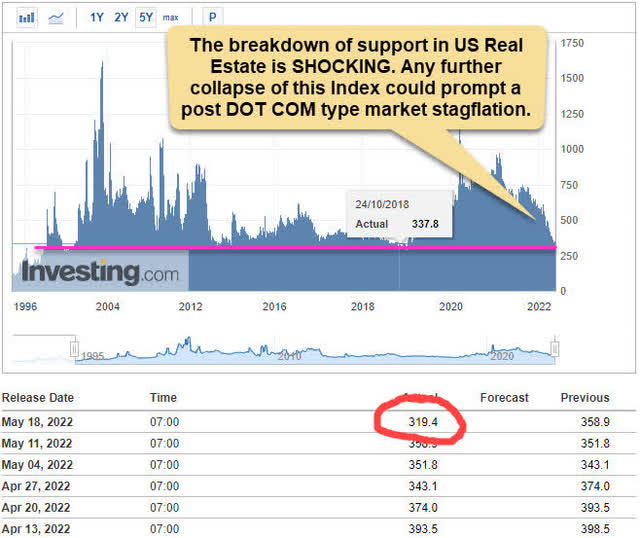

New mortgage demand collapses as most real estate investors are priced out of buying homes

Sharp declines in mortgage demand is indicative of a collapse in consumer confidence and willingness to believe the economy is going to continue to grow. The warnings from the US Fed, as well as signs that international market conditions are deteriorating quickly, have US consumers and property owners on edge – watching for the next shoe to drop for real estate and home prices (again).

Real Estate Investing Mortgage Demand

Source: investing.com

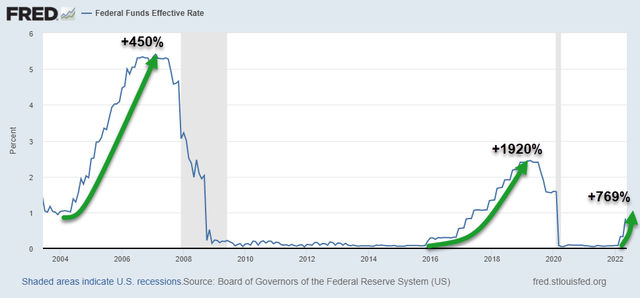

US Fed On Target For An 1100%+ Rate Increase Over 4+ months – Fastest In Recent History

The US Federal Reserve has continued to suggest further rate increases are necessary to help tame current inflation trends. By many conservative estimates, the US Fed is targeting levels at or above 2.0%. These extremely aggressive targets would represent the fastest and potentially largest rate increase in recent history on a percentage basis.

If the US Fed next raises interest rates by 0.50%, that would represent a 1100%+ rate increase in just 90 days. Rates moving to 2.0% or higher soon, will represent a 1500%+ increase over 4 to 5+ months.

Source: St. Louis Fed

Extreme Post-COVID Speculative Wave May Have Extreme Consequences

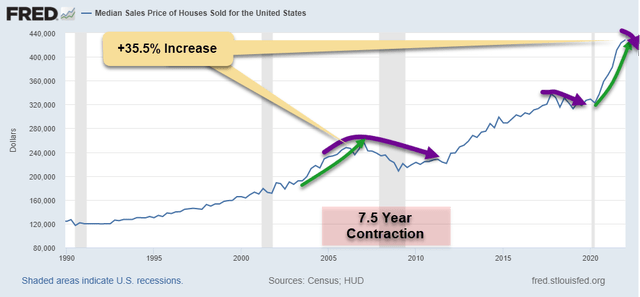

Inflation and many other economic issues are suddenly front-and-center for central banks and property investors across the globe. News that China’s real estate price levels continue to decline may be a very clear sign that China/Asia has peaked ahead of the US and other global markets. We’ve never seen anything like the sharp rally in global real estate price levels except for a brief period from 2004 to 2008 (see chart below).

Investment Home Prices

Source: St. Louis Fed

That rally ended with the Global Financial Crisis. Home prices declined nearly -20% from the peak in Q1:2007 to the bottom in Q1:2009. If history repeats, US home prices will fall more than -20% to -25% for real estate investors as history has a way of repeating.

US Equity Market May Not Follow Asset Prices Downward As Economy Shifts

I want to urge you to consider how capital works in a shifting global market environment. Capital is always seeking out the best, most opportunistic, instruments for future gains and protection against risks. Even when the markets were turning downward in 2009, a bottom set up in the US stock market long before other assets found their bottom in price. This same type of scenario may play out over the next 12 to 24+ months.

If my interpretation of market conditions is correct and the US Fed attempts to raise rates further to mitigate inflationary trends, it is likely that various asset classes, including real estate, ETFs, and individual sectors will unwind risks (as we are now seeing) and will possibly turn into future opportunities. What was overvalued in the past may turn into an incredible opportunity as capital shifts towards sectors/trends showing opportunities for future ROI.

The current market trends will present incredible opportunities for traders/investors that are able to protect capital, see and understand the risks and opportunities unfolding, and time their investments/trades properly in the markets.

In today’s market environment, it’s imperative to assess your trading plan, portfolio holdings, and cash reserves. Experienced traders know what their downside risk is and adapt as necessary. Successful traders manage risk by utilizing stop-loss orders, rebalancing existing positions, reducing portfolio holdings, liquidating investments, and moving into cash.

Managing risk and expectations for both investments in real estate and the stock market is the key for long-term success. Do this, and you can avoid the rollercoaster ride of doing nothing to protect your investments.

Successfully managing our drawdowns ensures our trading success. The larger the loss, the more difficult it will be to make up. Consider the following:

- A loss of 10% requires an 11% gain to recover

- A 50% loss requires a 100% gain to recover

- A 60% loss requires an even more daunting 150% gain to simply return to break even.

Recovery time also varies significantly depending upon the magnitude of the drawdown. A 10% drawdown can typically be recovered in weeks or months, while a 50% drawdown may take years to recover.

Depending on a trader’s age, they may not have the time to wait on the recovery or the patience. Therefore, successful traders know it’s critical to keep their drawdowns within reason. Most of them learned this principle the hard way.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.